Asset-Based Lending Market Growth Driven by SME Financing Demand 2032

Asset-Based Lending Market: Growth, Dynamics, Trends, and Forecast (2025–2032)

Market Overview

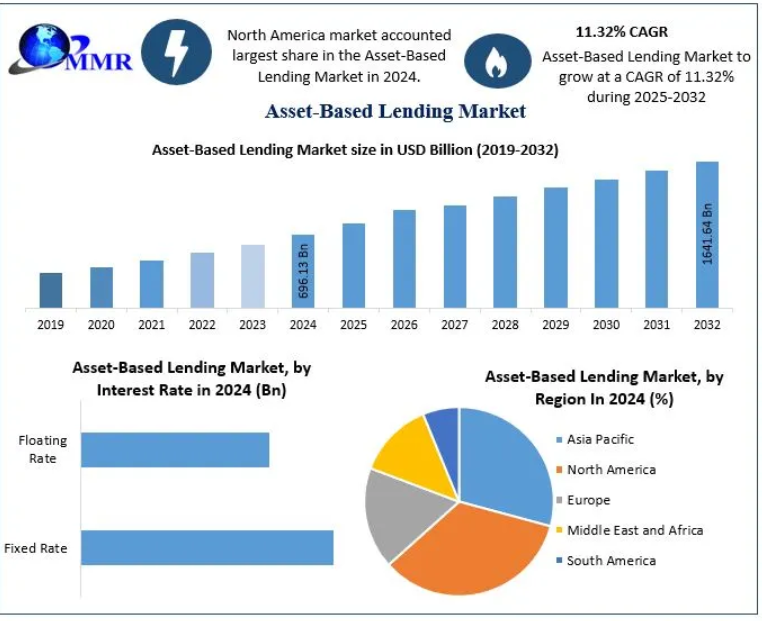

The global Asset-Based Lending (ABL) market was valued at USD 696.13 billion in 2024 and is projected to expand at a robust CAGR of 11.32% from 2025 to 2032, reaching approximately USD 1,641.64 billion by 2032. This strong growth reflects rising demand for flexible, collateral-backed financing solutions across businesses of all sizes, particularly small and medium-sized enterprises (SMEs).

Asset-Based Lending is a financing mechanism in which loans are secured against tangible or financial assets rather than relying primarily on the borrower’s credit profile or historical cash flows. Commonly pledged assets include accounts receivable, inventory, machinery, equipment, and real estate. Lenders assess the quality, liquidity, and marketability of these assets to determine loan eligibility and size.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/189641/

Research Methodology

The market size for asset-based lending has been evaluated using a bottom-up research approach, combining primary research (industry interviews, lender insights, and expert opinions) with secondary research (financial reports, regulatory data, and industry publications). This approach ensures accurate representation of market trends and segment-level growth dynamics.

How Asset-Based Lending Works

In asset-based lending, the loan amount is determined as a percentage of the appraised value of the pledged collateral, known as the advance rate. Advance rates vary depending on asset type and liquidity:

- Accounts receivable: Up to ~80%

- Inventory: Around ~50%

- Equipment and real estate: Based on valuation and resale potential

This structure allows businesses to convert illiquid assets into immediate working capital. Funds obtained through ABL are widely used for growth expansion, acquisitions, cash flow stabilization, refinancing existing debt, and operational restructuring.

Key Advantages of Asset-Based Lending

Enhanced Liquidity and Cash Flow Stability

One of the most significant benefits of asset-based finance is its ability to unlock liquidity. By monetizing balance-sheet assets, businesses gain predictable cash flows, making ABL especially attractive for:

- Fast-growing companies

- Businesses with seasonal revenue cycles

- Firms experiencing temporary cash flow constraints

This liquidity advantage enables organizations to stabilize operations and plan long-term growth more effectively.

Accessibility for Non-Investment-Grade Borrowers

Asset-based lending is particularly suitable for businesses that may not qualify for traditional cash-flow-based loans due to:

- Limited operating history

- Credit challenges

- Transitional business phases

By emphasizing collateral value instead of profitability metrics, ABL widens financing access for companies undergoing change or expansion.

Market Drivers

Easier Qualification Criteria Compared to Traditional Loans

Unlike conventional bank lending, which requires consistent cash flows and strict financial covenants, asset-based lending focuses primarily on collateral availability. Accounts receivable from creditworthy customers are especially favored, as they can be quickly converted into cash. Equipment and inventory further enhance eligibility, making ABL a more inclusive financing option.

This reduced dependency on credit scores and long financial histories significantly expands access to capital, fueling market growth.

Ability to Raise Larger Capital Amounts

Asset-based lending enables businesses—particularly startups and small enterprises—to secure substantial funding amounts that might otherwise be inaccessible. Entrepreneurs can consolidate financing needs into a single, asset-backed loan, reducing complexity and financial risk while supporting business launch and expansion.

Importance of Asset-Based Lending for SMEs

Small and medium-sized enterprises are the backbone of the global economy:

- Represent ~90% of businesses worldwide

- Contribute over 50% of global employment

- Generate up to 40% of GDP in emerging economies

Despite their importance, SMEs face major financing barriers. According to international estimates:

- Around 65 million MSMEs face an annual financing gap of USD 5.2 trillion

- Nearly 40% of formal SMEs lack adequate access to credit

Asset-based lending addresses this gap by providing alternative capital pathways, especially in regions where traditional bank financing remains limited. This makes ABL a critical tool in supporting SME growth, job creation, and economic development.

Market Landscape and Emerging Trends

Asset-based lending has evolved beyond receivables financing into a holistic asset valuation model, where lenders assess the entire asset portfolio of a business—including inventory, fixed assets, and future value potential.

Key trends shaping the market include:

- Integration of digital platforms for collateral monitoring

- Automation and data analytics for faster loan approvals

- Enhanced compliance and risk management tools

Impact of COVID-19

The COVID-19 pandemic accelerated the adoption of asset-based lending as many companies shifted from unsecured or cash-flow-based facilities to asset-backed credit lines. Industries with heavy inventory exposure—such as retail, wholesale, equipment rental, and food & beverage—particularly benefited from this transition. As a result, the pandemic had a net positive impact on ABL demand.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/189641/

Segment Analysis

By Type

Receivables Financing dominated the asset-based lending market in 2024 and continues to hold the largest revenue share. The segment is expected to grow at a CAGR of 9.1% during the forecast period, driven by its ability to:

- Improve working capital

- Reduce payment-delay risks

- Provide immediate liquidity

Inventory Financing is widely used by retailers and wholesalers to manage seasonal demand, while Equipment Financing supports capital-intensive industries such as manufacturing and construction.

By End User

Small and Medium-Sized Enterprises (SMEs) account for a significant share of the asset-based lending market due to limited access to traditional funding. ABL enables SMEs to leverage tangible assets rather than relying solely on creditworthiness.

Large enterprises also use ABL strategically, though their dependence is lower due to broader access to conventional financing sources.

Regional Insights

North America

North America dominated the global asset-based lending market in 2024, accounting for 37.8% of total revenue. The region is projected to grow at a CAGR of 10.12% through 2032, supported by:

- A mature financial ecosystem

- Strong regulatory frameworks

- High adoption of advanced lending technologies

The presence of established financial institutions and specialized ABL providers ensures efficient collateral valuation, loan structuring, and risk management, reinforcing regional leadership.

Market Scope

- Base Year: 2024

- Forecast Period: 2025–2032

- Market Size (2024): USD 696.13 Billion

- Market Size (2032): USD 1,641.64 Billion

Segmentation:

- By Type: Receivables Financing, Inventory Financing, Equipment Financing, Others

- By Interest Rate: Fixed Rate, Floating Rate

- By End User: Large Enterprises, SMEs

- By Region: North America, Europe, Asia Pacific, Middle East & Africa, South America

Key Market Players

Leading companies operating in the global asset-based lending market include:

- Lloyds Bank

- Barclays Bank PLC

- JPMorgan Chase & Co

- Wells Fargo

- HSBC Holdings plc

- Goldman Sachs Group, Inc.

- White Oak Financial, LLC

- Fifth Third Bank

- Santander Bank, N.A.

- KeyCorp

- Truist Financial Corporation

- Berkshire Bank

- SLR Credit Solutions

Conclusion

The Asset-Based Lending market is undergoing rapid expansion, driven by rising SME financing needs, flexible qualification criteria, and increasing adoption of technology-enabled lending solutions. As businesses seek alternative funding mechanisms to navigate economic uncertainty and growth challenges, asset-based lending is set to remain a cornerstone of modern commercial finance through 2032 and beyond.