Market Overview:

According to IMARC Group's latest research publication, "Osseointegration Implants Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", The global osseointegration implants market size was valued at USD 7,114.18 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 11,342.32 Million by 2033, exhibiting a CAGR of 5.05% from 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

How AI is Reshaping the Future of the Osseointegration Implants Market

- AI-driven imaging and CT scan analytics optimize pre-surgical implant planning by analyzing bone density with high precision, reducing placement errors by up to 30% and improving osseointegration success rates across dental and orthopedic applications.

- Machine learning integrated into CAD/CAM systems enables design of patient-specific implants with customized surface topographies, accelerating osseointegration timelines from months to weeks and significantly improving long-term implant stability.

- AI-enabled robotic-assisted surgery platforms enhance accuracy in drilling and implant placement during complex orthopedic and dental procedures, reducing surgical complications and post-operative recovery time by up to 20%.

- Predictive AI analytics help manufacturers optimize titanium alloy compositions and biocompatible coatings, improving corrosion resistance and bone-bonding properties of metallic implants, which command approximately 63.5% of the global market share.

- AI-powered remote monitoring systems track post-operative osseointegration progress in real time, enabling early detection of implant failure risks and reducing hospital readmissions, benefiting the leading hospital end-user segment that holds ~65.9% market share.

Download a sample PDF of this report: https://www.imarcgroup.com/osseointegration-implants-market/requestsample

Growth Factors in the Osseointegration Implants Market

- Increasing Aging Population and Orthopedic Demand: The global elderly population is rapidly expanding, directly elevating the incidence of bone-degenerative conditions. In the United States alone, approximately 58.5 million adults live with arthritis as of 2024 (CDC), projected to reach 78 million by 2040, with 25.7 million currently experiencing activity limitations. This creates a growing and predictable pipeline for joint replacement and osseointegration implant procedures.

- Advancements in Implant Technology and Biocompatible Materials: Innovations in implant surface coatings, 3D printing, and advanced biomaterials are substantially improving clinical outcomes. SINTX Technologies received a USPTO patent notice of allowance in September 2024 for methods to bond bioactive silicon nitride to zirconia-toughened alumina surfaces, expanding its portfolio to 16 U.S. patents. These developments reduce failure rates, shorten recovery periods, and broaden patient eligibility for osseointegration procedures globally.

- Rising Demand for Dental Implants and Aesthetic Oral Restoration: Growing awareness about oral health and the long-term functional and aesthetic advantages of osseointegration implants over removable dentures is driving dental segment demand. Dental Implants represent a significant product sub-segment, benefiting from increasing disposable incomes, the rise of dental tourism, and expanding dental clinic networks — particularly across Asia-Pacific and Latin American markets.

- Supportive Government Policies and Favorable Reimbursement Frameworks: Favorable reimbursement policies in North America and Europe are reducing out-of-pocket patient costs and making osseointegration implants more broadly accessible. Government healthcare investment in emerging economies — particularly across Asia-Pacific and Middle East & Africa — is expanding hospital infrastructure and surgical capacity, creating new growth corridors for the market.

- Expanding Healthcare Infrastructure in Emerging Markets: Rapid healthcare infrastructure development across Asia-Pacific, Latin America, and MEA is unlocking substantial new market opportunities. In GCC countries, regional healthcare spending is estimated to reach USD 135.5 Billion by 2027. Brazil alone performs approximately 70,000 hip arthroplasties annually (Brazilian Hip Society), representing a significant and largely unmet opportunity for osseointegration implant adoption in orthopedic care.

We explore the factors propelling the osseointegration implants market growth, including technological advancements, consumer behaviors, and regulatory changes.

Key Trends in the Osseointegration Implants Market

- Rising Prevalence of Bone-related and Dental Disorders: The surge in osteoarthritis, osteoporosis, and dental conditions is driving massive demand for osseointegration implants. WHO estimates that approximately 528 million people globally lived with osteoarthritis in 2019 — a 113% increase since 1990 — with 73% of sufferers aged 55 and above. Simultaneously, approximately 2 billion people suffer from dental caries in permanent teeth, creating sustained and growing need for osseointegration-based dental and orthopedic solutions.

- Technological Advancements in Implant Materials and Surface Science: Innovations in titanium alloys, ceramic composites, and 3D-printed personalized implants are reshaping the market. Osstem Implant's TSIII SOI implant (March 2024) introduced a super-hydrophilic UV-treated surface that reduced the osseointegration period from six months to approximately two months. Metallic materials dominate with approximately 63.5% share, driven by their superior biocompatibility, corrosion resistance, and mechanical strength in dental and orthopedic applications.

- Shift Toward Minimally Invasive Surgeries (MIS): Patients and surgeons increasingly prefer MIS techniques for osseointegration procedures, as they reduce recovery time, minimize tissue trauma, and lower complication risks. This trend is particularly pronounced in North America, which holds over 55.8% of the global market share, supported by advanced healthcare infrastructure, strong R&D investment, and robust reimbursement policies.

- Expanding Adoption of Bone-Anchored Prostheses: Bone-anchored prostheses lead the product segment, driven by increasing limb amputations due to trauma, diabetes, and vascular diseases. These implants offer superior stability and functional improvement over traditional socket-based prosthetics, making them the preferred choice for rehabilitation across both developed and developing markets, with ongoing innovation in materials further expanding clinical adoption.

- Rapidly Aging Global Population: Demographic aging is a fundamental structural driver of the market. In Europe, 21.3% of the EU's 448.8 million population was aged 65 or above as of January 2023 (European Commission). In Asia-Pacific, China's elderly population is projected to double to 366 million (26% of total) by 2050, systematically elevating the demand for orthopedic joint replacement and dental restoration procedures requiring osseointegration implants.

Leading Companies Operating in the Global Osseointegration Implants Industry:

- Bicon

- CAMLOG Biotechnologies GmbH

- CONMED Corporation

- Dentsply Sirona

- Envista Holdings Corporation

- Henry Schein, Inc.

- Institut Straumann AG

- Integrum

- Osstem Implant Co. Ltd.

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

Osseointegration Implants Market Report Segmentation:

Breakup By Product:

- Bone-Anchored Prostheses

- Dental Implants

Bone-anchored prostheses account for the majority of the product segment owing to their ability to provide superior stability, enhanced mobility, and improved quality of life for individuals requiring limb replacement.

Breakup By Material:

- Metallic

- Ceramic

- Polymeric

- Biomaterials

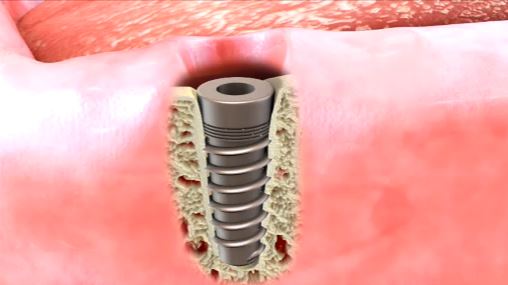

Metallic materials dominate the global market with approximately 63.5% share in 2024, driven by superior mechanical properties, corrosion resistance, and decades of clinical validation across dental, orthopedic, and maxillofacial applications.

Breakup By End User:

- Hospitals

- Ambulatory Surgical Centers

- Dental Clinics

Hospitals represent the dominant end-user category with approximately 65.9% market share in 2024, supported by government and private investments in hospital facilities, particularly in emerging economies.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa (United Arab Emirates, Saudi Arabia, Qatar, Iraq, Others)

North America holds the leading regional position with over 55.8% market share in 2024, underpinned by advanced medical technology adoption, an extensive R&D ecosystem, and favorable reimbursement environments. The United States accounts for 89.30% of the North American segment.

Recent News and Developments in the Osseointegration Implants Market

- February 2024: ZimVie Inc. launched the TSX Implant in Japan, significantly expanding its dental implant product portfolio in the Asia-Pacific region and reinforcing its strategic growth presence.

- September 2024: SINTX Technologies received a USPTO patent notice of allowance for methods to bond bioactive silicon nitride to zirconia-toughened alumina (ZTA) surfaces, expanding its intellectual property portfolio to 16 U.S. patents.

- March 2024: Osstem Implant launched its TSIII SOI implant featuring next-generation Super Osseointegration (SOI) surface treatment using UV and HEPES buffering agents, creating a super-hydrophilic coating that reduces the osseointegration period from up to six months to approximately two months.

- May 2023: Zimmer Biomet Holdings Inc. completed its acquisition of Ossis, a maker of customized 3D-printed hip replacement implants, reinforcing its portfolio and expanding its Asia-Pacific partnership presence.

- March 2023: Dentsply Sirona introduced the DS OmniTaper Implant System designed for a wide range of clinical applications, featuring an efficient drilling protocol and a pre-mounted TempBase component for immediate restoration, enhancing procedural workflows.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201-971-6302