Structural Heart Devices Market Positioned for Robust Transformation Through 2035 as Innovations Accelerate Adoption of Minimally Invasive Therapies

The Structural Heart Devices Market is undergoing a period of unprecedented transformation, shaped by rapid advancements in interventional cardiology, rising diagnoses of structural heart diseases, and the global shift toward minimally invasive solutions. Structural heart diseases—including valvular defects, cardiomyopathies, septal abnormalities, and congenital anomalies—represent a significant and growing global health burden. With aging populations expanding and diagnostic capabilities advancing, the incidence of these disorders continues to rise. Against this backdrop, structural heart devices have emerged as vital tools to restore cardiac function, reduce hospitalizations, and extend life expectancy for millions of patients worldwide.

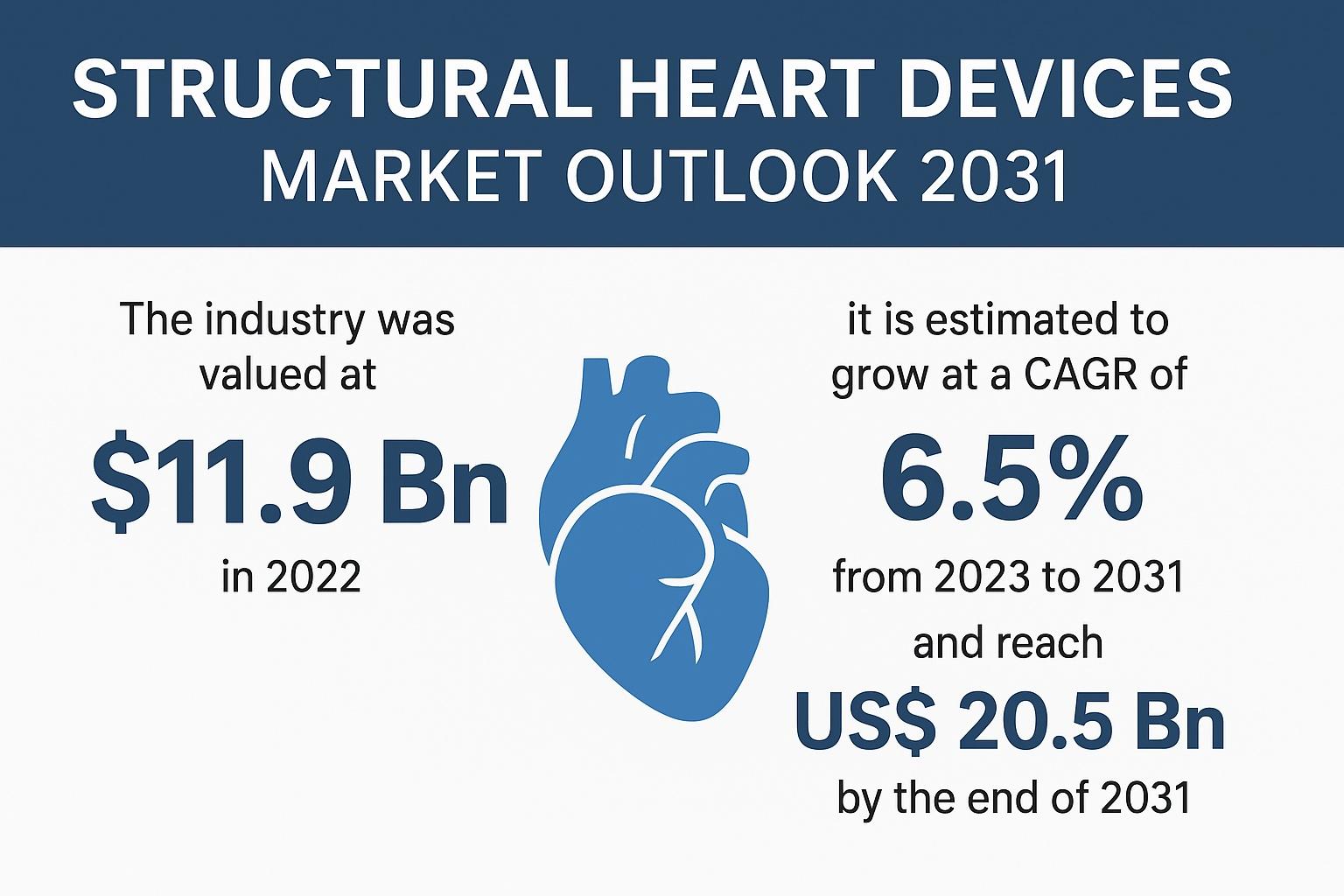

In 2022, the global market for structural heart devices was valued at US$ 11.9 billion, and it is forecast to reach US$ 20.5 billion by 2031, expanding at a CAGR of 6.5% from 2023 to 2031. North America remains the dominant region due to early adoption of breakthrough technologies, favorable reimbursement pathways, and strong presence of leading device manufacturers. However, Asia Pacific represents the fastest-growing region, driven by rising health expenditures, expanding hospital infrastructure, and increasing use of minimally invasive therapies.

This article explores the market’s evolution, core drivers, technological innovations, segmentation dynamics, competitive landscape, and regional outlook—offering a detailed view of why the Structural Heart Devices Market is positioned for robust expansion through 2035.

Growing Disease Burden Reinforces the Need for Advanced Structural Heart Therapies

Structural heart diseases have become a critical global concern due to their strong association with aging, lifestyle-linked risk factors, and improved diagnostic detection. Conditions such as aortic stenosis, mitral regurgitation, ventricular septal defects, and congenital anomalies collectively affect millions—and many cases go untreated due to lack of awareness or access to care.

Key Contributing Factors:

-

Aging Population:

As people age, calcification and degeneration of heart valves become more prevalent. Aortic stenosis and mitral valve disease are especially common among the elderly. -

Lifestyle-Linked Diseases:

Hypertension, diabetes, obesity, and chronic cardiovascular conditions contribute to valve deterioration and structural abnormalities. -

Improved Imaging and Diagnostics:

Widespread use of echocardiography, cardiac MRI, CT angiography, and AI-assisted diagnostic tools has increased detection rates of structural abnormalities. -

Congenital Heart Disease (CHD):

CHD is the most common congenital disorder. As survival rates increase due to better surgical and medical care, more adults require long-term structural heart interventions.

This combination of factors guarantees a consistent and rising demand for structural heart solutions such as occluders, annuloplasty devices, transcatheter valves, and mechanical or biological surgical valves.

Shift Toward Minimally Invasive Interventions is Transforming Patient Care

A defining characteristic of the Structural Heart Devices Market is the rapid shift toward minimally invasive, catheter-based interventions, offering reduced surgical risk and faster recovery times. This shift is most evident in procedures like:

Transcatheter Aortic Valve Replacement (TAVR)

TAVR has transformed the treatment landscape for aortic stenosis. Initially approved only for high-risk surgical candidates, TAVR is now used for intermediate- and low-risk groups as well. Studies have demonstrated superior or comparable outcomes to open surgery, driving widespread adoption.

Transcatheter Edge-to-Edge Repair (TEER)

Devices like Abbott’s MitraClip have become standard for patients with mitral regurgitation. TEER enables leaflet approximation without the need for open-heart surgery.

Septal Defect Closure Devices

Atrial septal defect (ASD), ventricular septal defect (VSD), and patent foramen ovale (PFO) occluders allow minimally invasive repairs, eliminating the need for cardiopulmonary bypass surgery.

Left Atrial Appendage (LAA) Occlusion Devices

LAA occluders help reduce stroke risk in atrial fibrillation patients who cannot tolerate anticoagulants.

The growing preference for catheter-based interventions—combined with improvements in imaging, procedural precision, and device reliability—continues to propel the market forward.

Technological Advancements Underpin Market Growth

Innovation remains at the heart of the Structural Heart Devices Market. Advances in materials, imaging techniques, device engineering, and hybrid cardiac procedures have made structural interventions safer, more effective, and more accessible.

Breakthrough Innovations Driving the Market:

1. Next-Generation Transcatheter Heart Valves

Modern valve designs are more durable, easier to deploy, and adaptable to various anatomical structures. These advancements increase procedural success and expand eligibility for patients previously considered poor candidates.

2. AI-Enhanced Imaging & Robotic Assistance

Real-time 3D imaging, machine-learning-based diagnostics, and robotic-assisted catheter navigation improve accuracy and reduce procedural risks.

3. Minimally Invasive Annuloplasty Rings

Flexible, adjustable annuloplasty systems enable precise remodeling of mitral or tricuspid valves through transcatheter approaches.

4. Hypoallergenic & Hemocompatible Materials

New biomaterials reduce the risk of inflammation, thrombosis, and device-related complications—critical factors for durability and long-term safety.

5. Personalized & Anatomically Adaptable Devices

Customization based on patient geometry leads to better outcomes and reduces device migration or paravalvular leakage.

Recent Industry Developments

Notable advancements include:

-

2024: FDA approval for Occlutech’s ASD Occluder for congenital defect closure.

-

2024: Integer Holdings acquired Pulse Technologies to enhance precision-engineered components for cardiovascular devices.

-

2023: Edwards Lifesciences announced the spin-off of its critical care business to focus on high-growth structural heart innovations.

These developments signify an industry intensifying its focus on innovation and regulatory progress.

Market Segmentation Insights

The Structural Heart Devices Market is diverse and includes a wide spectrum of devices used for both repair and replacement procedures.

By Product Type

1. Biological/Tissue Valves

Bioprosthetic valves made from animal tissue (porcine or bovine) offer durability with lower anticoagulation requirements. They dominate procedures in elderly patients.

2. Transcatheter Heart Valves

These valves drive the highest growth, fueled by the expansion of TAVR and TMVR (Transcatheter Mitral Valve Replacement).

3. Mechanical Heart Valves

Known for exceptional durability, mechanical valves require lifelong anticoagulation. They are preferred for younger patients.

4. Annuloplasty Devices

Used primarily in mitral and tricuspid repair, these rings or bands strengthen or reshape the valve annulus.

5. Occluders and Septal Closure Devices

Essential for treating congenital defects, these devices offer minimally invasive alternatives to open surgery.

6. Accessories

Includes introducers, delivery systems, sutures, and ancillary equipment supporting structural interventions.

By Procedure

1. Replacement Procedures

Includes TAVR, surgical valve replacement (SAVR), and transcatheter mitral or tricuspid replacement. Growing adoption of catheter-based replacements is the key trend.

2. Repair Procedures

Valve repair technologies, particularly TEER and annuloplasty, are gaining popularity due to improved longevity and lower risk compared to replacement.

By Indication

-

Valve Stenosis (especially aortic stenosis)

-

Valve Regurgitation (mitral regurgitation most prevalent)

-

Congenital Heart Defects (ASD, VSD, PFO)

-

Cardiomyopathy

-

Others, including tricuspid abnormalities and left atrial appendage dysfunction

Regional Outlook

1. North America

North America accounts for the largest share of the Structural Heart Devices Market due to:

-

Advanced healthcare infrastructure

-

Favorable reimbursement systems

-

High procedure volumes of TAVR and TEER

-

Presence of major players (Edwards, Abbott, Boston Scientific)

High awareness among clinicians and patients also drives early adoption of newer structural heart technologies.

2. Europe

Europe remains an innovation hub with strong collaboration between industry and research institutes. Countries like Germany, the U.K., and France lead in the number of structural interventions performed. EU MDR regulations enhance product safety but also increase time to market.

3. Asia Pacific

Asia Pacific presents the fastest-growing opportunity. Key drivers include:

-

Growing incidence of cardiovascular diseases

-

Rising hospital upgrades and digital health penetration

-

Increasing adoption of minimally invasive cardiac therapies

-

Expanding insurance coverage in India, China, and Southeast Asia

The region’s rapidly aging population will further amplify the demand for structural heart devices.

4. Latin America

Growth is moderate but rising due to:

-

Increasing availability of interventional cardiology centers

-

Public health initiatives supporting cardiovascular care

However, access and affordability remain challenges in some countries.

5. Middle East & Africa (MEA)

MEA shows steady growth, supported by:

-

Improved hospital infrastructure in GCC countries

-

Rising prevalence of lifestyle diseases

-

Growing adoption of TAVR and septal defect closures in urban centers

Competitive Landscape

The Structural Heart Devices Market is dominated by global players investing heavily in R&D, regulatory approvals, and next-generation device innovation.

Key Companies Include:

-

Medtronic plc

-

Abbott Laboratories

-

Boston Scientific Corporation

-

Edwards Lifesciences Corporation

-

LivaNova PLC

-

Lepu Medical Technology (Beijing) Co. Ltd.

-

LifeTech Scientific

-

CryoLife Inc.

-

Micro Interventional Devices Inc.

Each company is actively pursuing strategies such as acquisitions, product launches, and research collaborations to strengthen their global market position. The competitive focus remains on durability, ease of delivery, anatomical compatibility, and improved long-term outcomes.

Future Outlook: Structural Heart Devices Market Toward 2035

The period through 2035 will be defined by expanding transcatheter interventions, AI-assisted procedural support, enhanced imaging modalities, and the rise of personalized structural heart therapy.

Key Trends Shaping the Future:

-

TMVR and TTVR (Tricuspid valve replacement) will emerge as major growth areas.

-

Structural interventions will increasingly be performed in hybrid OR–catheter labs.

-

Device manufacturers will use real-world evidence (RWE) to accelerate approvals.

-

Emerging economies will dominate volume growth.

-

Robotic and AR-guided structural interventions will enhance precision.

With steady demand, technological excellence, and expanding patient eligibility, the Structural Heart Devices Market is poised for sustainable long-term growth.