Automotive Lead Acid Battery Market Size, Share and Growth Forecast 2025-2033

Market Overview:

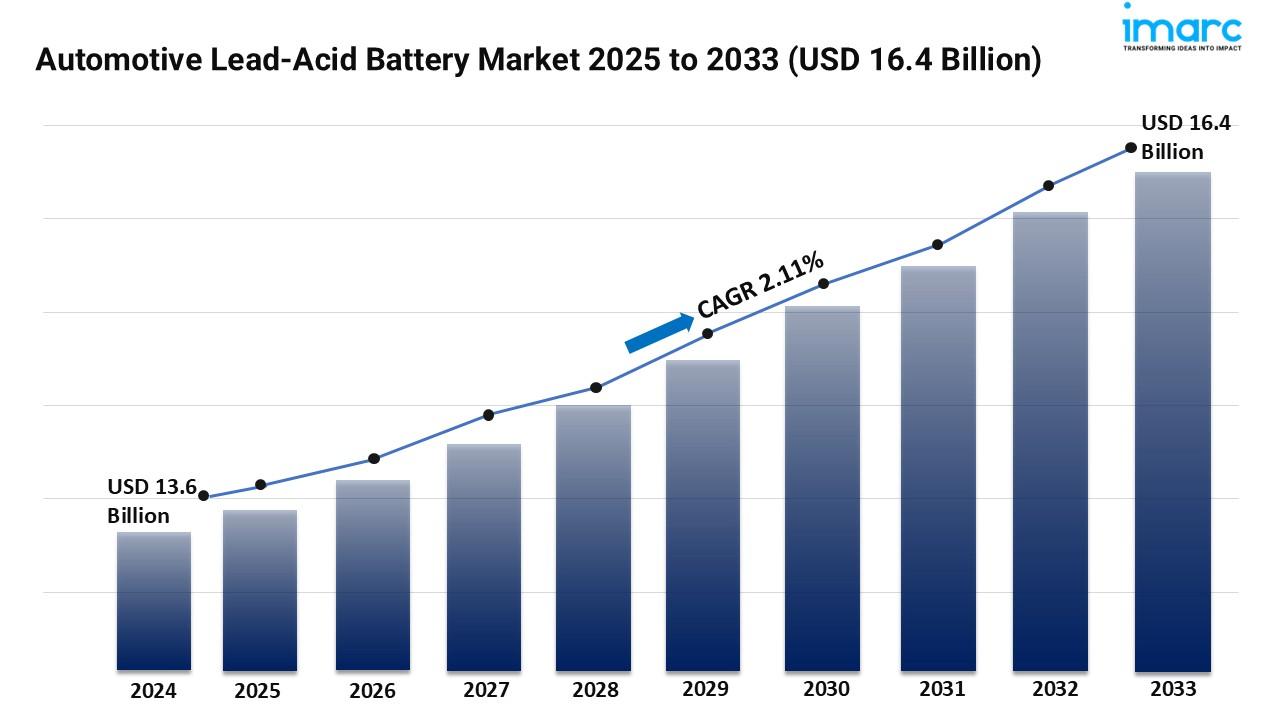

The automotive lead-acid battery market is experiencing rapid growth, driven by Sustained Demand in Aftermarket and Replacement Cycles, Dominance in Conventional Vehicle SLI Applications and Integration into Start-Stop Micro-Hybrid Vehicles. According to IMARC Group’s latest research publication, “Automotive Lead-Acid Battery Market : Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033“, The global automotive lead-acid battery market size reached USD 13.6 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 16.4 Billion by 2033, exhibiting a growth rate (CAGR) of 2.11% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/automotive-lead-acid-battery-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends And Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Automotive Lead Acid Battery Market:

- Sustained Demand in Aftermarket and Replacement Cycles

The growth of the automotive lead-acid battery market is dependent on the inelastic demand for replacement lead-acid batteries in the aftermarket segment. Regardless of vehicle type, the usable lifetime of lead-acid batteries is limited, as they degrade due to extreme temperatures and repeated charge-discharge cycles, resulting in a replacement demand in the aftermarket segment. Because of the size of the worldwide motor vehicle market (which exceeded 92 million motor vehicle sales in 2010), a large and predictable replacement market is in place. Replacement sales amount to a large percentage of lead acid sales in the automotive markets of mature economies. A majority of established manufacturers are focused on this relatively predictable cyclic pattern of use and have an array of new products, like the improved Valve Regulated Lead Acid (VRLA) technology, to supply the huge aging global conventional vehicle fleet.

- Dominance in Conventional Vehicle SLI Applications

Lead-acid batteries continue to dominate the Starting, Lighting and Ignition (SLI) requirements of the huge majority of new and replacement Internal Combustion Engine (ICE)-driven vehicles across the world due to the low cost and well-proven technology. SLI now represents a major portion of the lead-acid battery market, often over 50%. Despite the increased production and use of EVs, the mass market production of conventional vehicles continues to increase, particularly cars and light trucks in developing countries in the Asia-Pacific, where over half of the global annual passenger car production is manufactured. This high volume means that a very high volume of lead-acid batteries will be sold as OE parts. No other battery technology has been able to compete on price in this mass market.

- Integration into Start-Stop Micro-Hybrid Vehicles

Increased penetration of advanced fuel economy technologies in the market, including the rapidly growing start-stop technology, is generating demand for more premium lead-acid batteries. Start-stop technology is a micro-hybrid that automatically turns off the engine when the vehicle is idling and quickly starts it again when the driver steps on the accelerator. This greatly increases the number and depth of discharge/charge cycles seen by the battery, and advanced EFB and AGM batteries are being introduced to meet this demand. These high-technology lead-acid batteries have better cycle life compared to conventional flooded batteries. They are beginning to penetrate the market, reaching a reduced fuel consumption (an improvement of up to 10%) and a higher niche for premium lead-acid batteries in the current generation of eco-friendly conventional automobiles.

Key Trends in the Automotive Lead Acid Battery Market

- The Rise of Advanced AGM and EFB Batteries

The large trend in the marketplace is the production and sales of Advanced Flooded Batteries (EFB) and Absorbent Glass Mat (AGM) battery configurations for the high level of automotive electronics and micro-hybrid applications. AGM batteries use a glass mat separator that absorbs the electrolyte. These batteries are spill-proof and are more ruggedized to work under extreme vibration and harsh chemical circumstances compared with flooded batteries. This sector is a particular focus for large manufacturers that are retrofitting facilities for the production of high electronic load and start-stop systems, which are finding their way into even entry-level vehicles. For example, AGM batteries are mandated in vehicles that happen to have regenerative braking since high-rate charge acceptance is required in order to absorb the energy that is created during braking. Hence the advanced lead-acid battery is the battery-of-choice for modified performance, and higher spec conventional vehicles.

- Pioneering Highly Efficient, Closed-Loop Recycling

The automotive lead-acid battery industry benefits from a highly advanced and efficient closed-loop recycling system that has been driven by stringent regulatory requirements imposed by governments. Extended Producer Responsibility (EPR) schemes are mandated by many large governments and require battery producers to be responsible for battery collection and recycling. This has led to commercial recycling processes that recover over 95% of the lead and plastic components. The scope of ecodesign helps ensure that the business can convert waste products into a properly secured form of raw material for future recycling, which is increasingly important in uncertain commodities markets. The largest producers have invested in advanced collections networks and smelting technology, allowing them to reduce their reliance on newly mined lead; they claim that the lead-acid battery is one of the most successful circular economy products available.

- Use of Lead-Acid Batteries as Auxiliary Power in EVs

The 12-volt lead-acid battery continues to be the dominant technology for auxiliary electronics in most electric and plug-in hybrid vehicles, although the vehicle's drivetrain is powered by lithium-ion battery technology. The 12-volt subsystem is used to power low-voltage vehicle components such as door locks, airbags, emergency call systems, and the high voltage battery system isolation contactors. The lead-acid battery is smaller than a conventional one and, with tens of millions of EVs now sold each year globally and nearly all using a compact lead-acid battery for safety and vehicle control systems, the lead-acid battery is well positioned as an intrinsic part of the electrification evolution. Their products are currently being adapted to meet the low-voltage power management needs of the electrical systems for all types of vehicle platforms.

Leading Companies Operating in the Global Automotive Lead-Acid Battery Industry:

- C&D Technologies Inc.

- Clarios

- CSB Energy Technology Co. Ltd (Showa Denko K.K.)

- East Penn Manufacturing Company

- EnerSys

- Exide Industries Ltd.

- GS Yuasa Corporation

- Koyo Battery Co., Ltd.

- Leoch International Technology Ltd

- PT. Century Batteries Indonesia

- Robert Bosch GmbH

- Thai Bellco Battery Co. Ltd.

Automotive Lead-acid Battery Market Report Segmentation:

By Vehicle Type:

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

- HEV Cars

Commercial vehicles represented the largest segment due to their higher power requirements and the need for reliable, cost-effective batteries in applications, such as trucks, buses, and heavy-duty vehicles.

By Product:

- SLI Batteries

- Micro Hybrid Batteries

SLI batteries accounted for the largest market share as they are essential for starting, lighting, and ignition functions in both passenger cars and commercial vehicles.

By Type:

- Flooded Batteries

- Enhanced Flooded Batteries

- VRLA Batteries

Flooded batteries exhibit a clear dominance in the market on account of their established presence, cost-effectiveness, and suitability for a wide range of automotive applications.

By Customer Segment:

- OEM

- Replacement

OEM holds the biggest market share as it is the primary consumer of lead-acid batteries for new vehicle production.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific enjoys the leading position in the automotive lead-acid battery market. This can be accredited to its robust automotive manufacturing industry, especially in countries like China and India.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1–201971–6302